In the global economy today, the challenges posed by financial risk management while driving business momentum are present for companies of all sizes.

Bank guarantees have become critical instruments to facilitate cross-border and cross-sector commercial engagement within a framework of financial security and mutual trust attached to all parties involved.

This blog will help you unravel the relative advantages and disadvantages of bank guarantees to deliver a managerial note to organisations wishing to smarten their financial strategies and widen their business horizons.

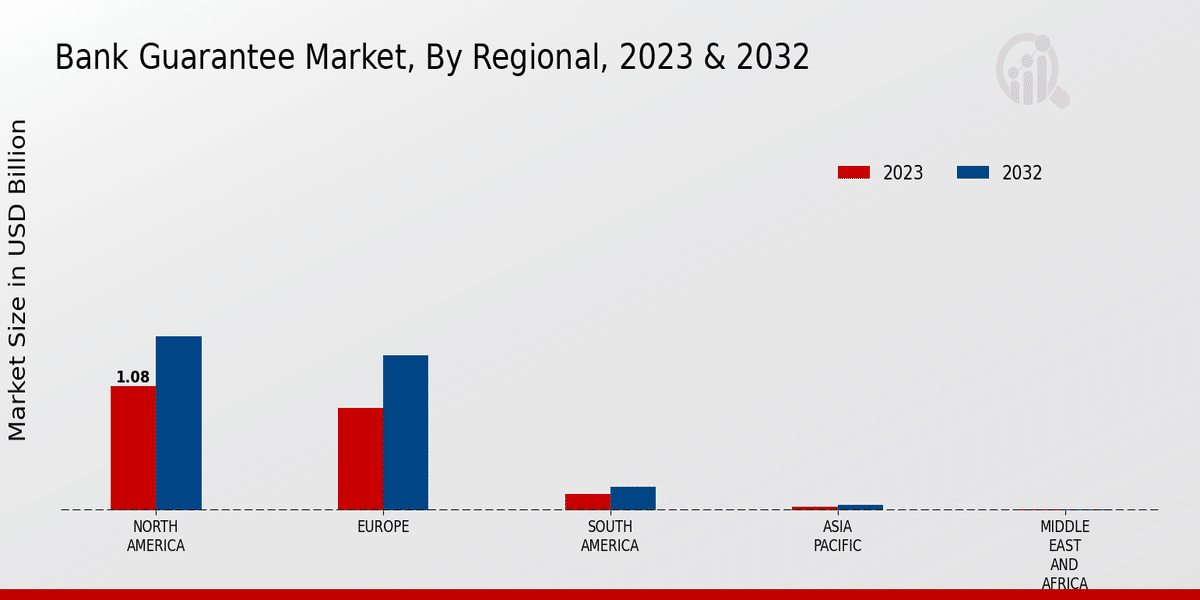

North America held the largest revenue share regionally in 2023 with a revenue share of about 36.7%. Europe was the second-largest market, accounting for approximately 30.2% of revenue.

What is a Bank Guarantee?

A bank guarantee is a financial document, under which a bank agrees to meet the obligation of a client in case of default. In international trade, bank guarantees reduce the trust deficit between parties in different countries through reassurance that payments would be made or contractual obligations would be met in case of default on one side or the other, thereby enabling confidence and carrying out cross-border transactions that otherwise could be too risky.Global Bank Guarantee Overview

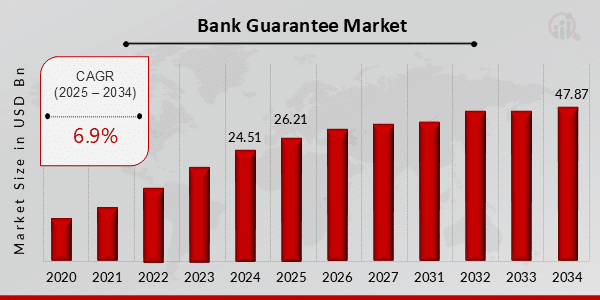

As per Market Research Future Reports, the Bank Guarantee Market Industry is expected to grow from 26.21 billion USD in 2025 to 47.87 USD billion by 2034, showing a compound annual growth rate (CAGR) of 6.9% during the forecast period (2025 – 2034).Advantages of Bank Guarantee

1. Enhanced credibility and trust

Besides enhancing credibility, bank guarantees imbue a business with additional trust. Companies look more trustworthy when a credible financial institution backs them. A 2023 survey conducted by the International Chamber of Commerce indicates that companies with bank guarantees are 37% more likely to win international contracts compared with companies that do not have such guarantees.2. Risk mitigation

The transferring of financial risk from the beneficiary over to the bank is merely risk management in disguise. This acts as insurance for more high-value transactions where the risks are high. If used correctly, bank guarantees bring down the risk of nonpayment by up to 78% in cross-border trade.3. Access to large contracts

By providing bank guarantees, smaller enterprises are in a position to bid for larger contracts that otherwise would be out of their reach financially. Reports from small business association officials show that, thanks to bank guarantees, SMEs could handle a 40% increase in contract value.4. Performance enhancement

Bank guarantees would enhance the contractor’s and supplier’s performance standards. Once a company knows that a financial institution is backing their performance with a guarantee, the probability that the company will fulfill or even exceed its contractual obligations is quite high. Research by the International Project Management Association states that performance guarantees add to an impressive 31% more timely completions of projects than projects that do not have performance guarantees.5. Lower interest rates compared to loans

When compared to loans, bank guarantees are likely to be a better option. While a short-term business loan charges 7%-12% interest, bank guarantee fees are charged at 0.75%-2.5% annually. Because of this, bank guarantees are financially favourable in most cases over direct financing options.6. Regulatory compliance

In many industries, bank guarantees support businesses in fulfilling regulatory requirements. In this case, the construction, real estate development, and energy sectors see bank guarantees being demanded to prove financial capability and commitment. Regulatory compliance through bank guarantees has reduced legal disputes in their subsequent steps and processes by 67% in highly regulated sectors.